Introduction

Selling mineral rights can offer significant financial returns, especially if your property contains valuable resources like oil, gas, or minerals. However, alongside the financial benefits, it’s important to understand the tax implications. One of the key concerns is the capital gains tax that applies to the profit made from selling those rights. Knowing how the IRS treats this type of income can help you make informed financial decisions and avoid unexpected liabilities.

What Are Mineral Rights?

Mineral rights refer to the ownership of subsurface resources. These rights can be sold or leased separately from the land. When you sell your mineral rights, you transfer ownership of these underground resources to a third party, typically a mining or energy company. This sale can result in a large lump-sum payment, which may be subject to capital gains tax on mineral rights sale if it qualifies under IRS rules.

Capital Gains Tax Basics

Capital gains tax applies to the profit earned from selling a capital asset, such as property, stocks, or—in this case—mineral rights. The amount of tax you owe depends on two main factors: how long you held the rights and your total income level.

- Short-Term Capital Gains: If you held the mineral rights for one year or less before selling them, any gain is considered short-term. This type of gain is taxed at your ordinary income tax rate.

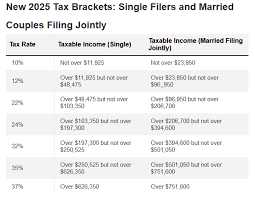

- Long-Term Capital Gains: If you held the rights for more than one year, the gain is considered long-term and is typically taxed at a lower rate—0%, 15%, or 20%, depending on your income bracket.

Calculating Capital Gains

To determine how much capital gains tax you owe, you need to calculate your capital gain:

Capital Gain = Sale Price – Cost Basis

- Sale Price: The total amount you received from selling your mineral rights.

- Cost Basis: What you originally paid to acquire the rights. If you inherited them, the cost basis is usually the fair market value at the time of inheritance.

For example, if you inherited mineral rights valued at $50,000 and sold them for $100,000, your taxable capital gain would be $50,000.

Reporting the Sale

The sale of mineral rights must be reported on Schedule D of your federal tax return. You may also need to fill out Form 8949, which provides detailed information about the asset sold, including dates, amounts, and the gain or loss.

Make sure to keep proper documentation, such as:

- Sale contracts

- Proof of original acquisition

- Closing statements or legal records

These documents are essential for verifying your cost basis and supporting your tax filings.

When to Consult a Tax Professional

While it’s possible to handle the tax reporting on your own, consulting with a tax advisor is strongly recommended—especially if the transaction is large or involves inherited rights. A professional can help you identify any possible deductions, correctly calculate your gain, and file the appropriate forms.

Final Thoughts

The sale of mineral rights can be a lucrative financial move, but it comes with tax responsibilities you can’t ignore. Understanding how capital gains tax applies will help you stay compliant and possibly reduce your overall tax burden. Proper planning and advice can make a big difference when managing your mineral assets.